Press releases and news updates from Manheim.

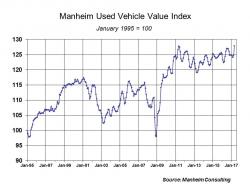

Wholesale used vehicle prices (on a mix-, mileage-, and seasonally adjusted basis) increased 1.1% month-over-month in June. This brought the Manheim Used Vehicle Value reading to 129.3, which was a record high for the second consecutive month and represented a 2.5% increase from a year ago.

On a year-over-year basis, the mid-sized car category saw the largest decline (down 2.1%) in June, while pickups and vans saw gains greater than the overall market.

Like May, the June index result challenges concerns that increasing wholesale supplies from near-peak off lease volumes and rising rental volumes would lead to rapidly declining used car values. Instead, strong retail demand for recent model year used vehicles is encouraging dealers to buy more vehicles from auction heading into the summer. The increased demand is more than offsetting the higher supply.

New vehicle market continues to struggle in 2017. Franchised dealers have had more than 4 million new units in stock for the last five months. June new vehicle sales volume slipped 3% year-over-year over the same number of selling days as June 2016. A majority of the decline can be attributed to slippage in car sales (down 13% year-over-year) while light truck sales were positive in June, up 4% year-over-year. New vehicle sales year-to-date are down 2% compared to last year.

Combined rental, commercial, and government purchases of new vehicles were down 13%, due primarily to a sharp decline of new sales into rental (down 22%). Retail sales were down 0.7% in June.

Used CPO sales softened in June. CPO sales fell slightly in June (-0.8%) after increasing substantially in May. Year-to-date CPO sales are up 1.3%. CPO sales of light trucks jumped 7% as increasing SUV/CUV/pickup inventory coming off-lease is lining up well with consumer demand. The passenger car share of CPO sales came in at 49% for June, as SUV/CUV/pickups began to dominate just as they have since 2013 in the new vehicle market.

Rental risk pricing eases on higher volume. The average price for rental risk units sold at auction in June was down 4% year-over-year; rental risk prices were up 0.2% compared to May.

SUV/CUVs accounted for 32% of rental risk sales in June of this year versus 30% last June. The share of compact cars fell from 25% to 23%. Average mileage for rental risk units in June (at 40,600 miles) was 2% below a year ago.

The U.S. economy remains strong. First-quarter GDP growth was revised up to 1.4% from the previous estimate of 1.2%. The second quarter is likely to come in stronger at a level of growth experienced throughout this expansion. Consumer confidence increased in June, snapping two months of declines following March’s 16-year-high reading. A strong and steady labor market combined with low interest rates enabled strong consumer demand for vehicles in the second quarter, but tempting values on a high-quality supply of used vehicles encouraged many consumers to choose used over new.

{kind=link}